The date of loss (DOL) in a property insurance claim is one of the fundamental elements that influence the entire process of claim settlement. Yet, it’s often overlooked or misunderstood by policyholders. In this guide, we’ll explore what the date of loss means, why it’s vital to have an accurate date, how it should align with weather data, the relevance of your policy coverage period, and common mistakes to avoid.

Importance of Having an Accurate Date of Loss

The date of loss holds more significance than a mere timeline point; it influences numerous aspects of an insurance claim. An accurate date is vital for policy compliance, as insurance policies often demand timely claim reporting linked to this date. This also impacts coverage determination, requiring the loss to fall within policy dates. Legal dimensions, such as statutes of limitations for lawsuits against insurers, are also tied to this date. Errors or discrepancies in this date can lead to complications, delays, or even the denial of a claim.

Understanding the date of loss isn’t just about following procedures; it’s about securing the rightful value of your claim. The value of the loss may vary depending on the date, impacting the settlement amount. In scenarios involving weather-related damages, such as storms or hurricanes, aligning the date of loss with weather data becomes crucial for both verifying the claim and determining the cause of damage. With a dispute, accurate weather records can be pivotal. In essence, the date of loss serves as the foundation upon which the claim is built, influencing everything from timelines to valuation, and ensuring its accuracy is paramount to a successful claim process.

Aligning the Date of Loss with Weather Data

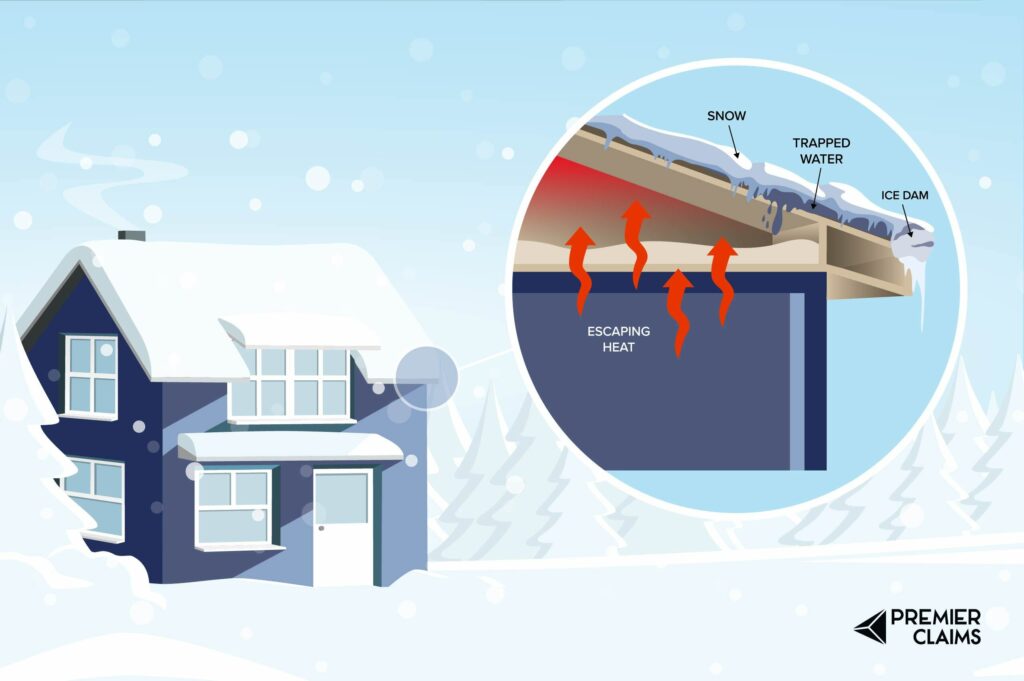

In many property damage claims, particularly those related to storms, hurricanes, hail, or other weather events, aligning the date of loss with the corresponding weather data becomes a significant step in the process. Here’s why:

Verifying the Claim

Weather records play an essential role in confirming the occurrence of a weather event on the claimed date of loss. Accurate alignment between the date and weather conditions can strengthen the credibility of the claim.

Determining the Cause of Damage

Accurate weather data helps in pinpointing the specific cause of damage, such as wind, rain, or hail. This alignment becomes especially important in disputes where weather conditions may be contested.

Professional Consultation

Engaging meteorologists or weather experts may be necessary to ensure the alignment of the date of loss with actual weather conditions. This expert input adds authority to the claim.

Legal Implications

In some cases, weather data alignment can have legal consequences, especially if fraudulent claims are suspected. Authentic weather records linked to the date of loss can help in resolving such legal issues.

Public Sources and Technologies

You can utilize various public weather sources and technologies, including satellite imagery and meteorological reports, to corroborate the date of loss with weather events. tools help in building a robust claim.

Aligning the date of loss with weather data is not just a validation step; it’s a comprehensive approach to establishing the authenticity, cause, and legal standing of a claim. The correct alignment ensures that the claim reflects the reality of the event, avoiding potential disputes or misunderstandings.

Knowing Your Policy Coverage Period

Understanding the coverage period of your insurance policy goes beyond merely knowing the start and end dates; it encompasses several crucial aspects:

Eligibility for Coverage

The date of loss must fall within the policy’s effective dates to be eligible for coverage. Any loss outside this period may lead to claim denial.

Renewal Considerations

If the loss occurs near the renewal or expiration date of the policy, special attention must be paid to ensure the claim falls within the correct policy period. A slight discrepancy can have significant implications.

Understanding Exclusions and Endorsements

The policy’s terms might change over time, affecting coverage for specific perils based on the date of loss. Being aware of these changes helps in avoiding surprises during the claim process.

Policy Extensions and Transitional Periods

Some policies may have extensions or transitional periods that might affect the coverage. Understanding these nuances ensures that the claim is handled appropriately.

Impact on Future Coverage

The reporting of a loss within the policy period might have implications for future coverage, affecting premiums or eligibility for renewals.

Knowing your policy’s coverage period is not just a matter of compliance; it’s an integral part of managing your insurance effectively. It determines the eligibility, scope, and even the future implications of a claim. Attention to this detail helps in avoiding unnecessary challenges and paves the way for a smoother claim experience. If you have questions on property insurance policy and coverage, submit your policy review questions with our legal team.

Common Claim Mistakes

Navigating the date of loss in an insurance claim might seem straightforward, but it’s a complex aspect that can lead to several mistakes. Here are some common pitfalls that policyholders, and even professionals like public adjusters, may encounter:

Using the Date of Discovery Instead of the Date of Loss

Mistaking the date of discovery for the date of loss when it doesn’t apply is a frequent error. This can lead to confusion and potential disputes, especially if the damage occurred much earlier than when it was discovered.

Failing to Consider the Policy Effective Date

Selecting the date of loss without considering the policy’s effective date may lead to a denied claim. The loss must fall within the coverage period, and ignoring this essential factor can have costly consequences.

Missing Proof of Loss Deadline

The proof of loss deadline is when policyholders submit a formal statement to their insurer about claimed loss. The deadline varies based on policy type, insurer, and jurisdiction. Mistakes risk reduced payouts or claim denial.

Using an Incorrect Date of Loss for Gradual Damage

In cases of gradual damage, such as slow water leaks, using an incorrect date of loss can complicate the claim process. Identifying the actual date of damage in such scenarios requires careful consideration and may need professional evaluation.

Ignoring Weather-Related Evidence

Lack of weather-related evidence can lead to disputes or claim denials, particularly in claims involving weather events. Proper alignment of weather data with the date of loss is vital.

Overlooking Policy Timelines

Different insurance policies may have varying timelines for reporting and other processes tied to the date of loss. Ignoring these specific timelines can lead to rejection or complications in the claim.

To sidestep these errors linked to the date of loss, focus on detail, policy awareness, and potential expert advice. Precision and adherence in this area facilitate a successful claim process, while missteps can trigger delays, conflicts, and claim rejections.

The date of loss is a seemingly simple yet profoundly influential factor in property insurance claims. It’s a cornerstone that supports compliance, coverage determination, damage valuation, and legal considerations. Understanding its definition, importance, weather alignment, policy period, and common mistakes helps policyholders navigate property insurance claims successfully.

Read More Trending Articles